Getting your small business payroll right!

It’s not easy for small business owners to keep up with all the legislation of payroll and workplace pensions. The costs have gone up and up with minimum wage and living wage increases, plus the costs of the workplace pension – employers can certainly do without receiving penalties for getting their payroll submissions wrong. However, when you’re busy trying to juggle lots of tasks, payroll is one of those that’s easy to get wrong.

How to get Payroll right:

Minimum Wage & Living Wage Rates

Every member of staff is entitled to the equivalent of a minimum hourly rate for the work they do for you. The rate depends on their age – apart from an Apprentice. The information below is from the HMRC website where there is more information on this:

Age 21 and Over – current rate £11.44/hr – 1st April increasing to £12.21

Age 18 to 20 – current rate £8.60/hr – 1st April increasing to £10.00

Age Under 18 – current rate £6.40/hr – 1st April increasing to £7.55

Apprentice – current rate £6.40/hr – 1st April increasing to £7.55

Calculating and Processing Payroll Wages

As well as calculating and processing pay and deductions, then assessing workplace pension contributions, an RTI (Real Time Information) report called an FPS (Full Payment Submission) must be sent to HMRC on or before every pay day, but did you know there is an additional monthly EPS (Employer Payment Summary) that has to be sent in certain circumstances.

For example

– To reclaim statutory payments such as maternity and paternity pay.

– To claim the £5,000 Government Employment Allowance.

– To reclaim Construction Industry Scheme (CIS) deductions as a LTD Company.

– To tell HMRC that you haven’t paid someone this month etc

More information on all of the above can be found on the HMRC Running Payroll website.

Workplace Pensions

There are many pension providers around, all offering different benefits. The way the contributions are calculated are also different and it’s important that you get the setup of these correct in your payroll software otherwise these deductions will be wrong which would cost you and your employee a lot of unnecessary money.

For example, some pensions calculate on all of an employees pay, whereas others, such as NEST don’t start generating contributions until pay has met the ‘qualifying earnings’ which is currently equivalent to £6,240 per year / £520 per month / £120 per week in 2024/25 tax year.

There are minimum percentage amounts that need to deducted from the employees pay if they are earning above the threshold and the employer has to also pay a minimum amount. In April 2025, this will be 5% for the employee and 3% for the employer, so that a total of 8% is being paid into the employees pension pot.

You can find out more about this on The Pension Regulator website.

Payroll Related Fines and Penalties

Forgetting to submit an RTI during the month is an automatic £100 penalty from HMRC if you have less than 10 employees – its double this if you have between 10 and 49 employees. Failing to pay the reported liability payments to HMRC by the dead line date will also incur interest penalties.

More painful is The Pension Regulator penalties. If you fail to assess and report your workplace pension obligations – you will be looking at a minimum £400 fixed penalty with a possible additional DAILY escalating penalty from £50 upwards.

Don’t let your name be in the Name and Shame list of employers that have been given these fines https://www.thepensionsregulator.gov.uk/en/document-library/enforcement-activity/penalty-notices

If you’re a small business in the Telford area and struggling to process your own payroll, if we do your bookkeeping – why not let Lady of Ledger Bookkeeping do this for you as well – contact us now for a quote by emailing us on info@ladyofledger.co.uk

Read Less...

It’s not easy for small business owners to keep up with all the legislation of payroll and workplace pensions. The costs have gone up and up with minimum wage and living wage increases, plus the costs of the workplace pension – employers can certainly do without receiving penalties for getting their payroll submissions wrong. However,

Read more…

Postponement is not just for Christmas – Workplace Pensions

When an Employer gives an employee an additional payment to their normal wage or salary, such as a Christmas bonus or overtime payment for additional hours to cover a busy period, this may trigger the requirement to auto enrol them into the workplace pension scheme. However, postponement may be an option in this situation.

Eligibility:

– There must have been at least one pay period between any previous postponement with that employee, and the current increased earning pay period.

– The postponement period can be UP TO a maximum of three months – but could be as little as one week, if weekly paid.

– A letter must be issued to the employee to explain what has been done.

For example:

Julia normally earns £800 per month in her part time work. In December pay, her employer wants to give her a Christmas bonus of £200, but this will trigger the Auto Enrolment threshold to enrol her. Her employer uses a one-month postponement period, issuing a letter to Julia to explain what he has done.

In January, Julia is back to her normal £800 per month, so is back under the auto enrolment threshold and postponement ends. Her February pay is the normal £800. In March, she is asked to do a small amount of overtime which would again take her over the threshold, but postponement could be used once again, as there was at least one clear pay period between these postponements.

Read Less...

When an Employer gives an employee an additional payment to their normal wage or salary, such as a Christmas bonus or overtime payment for additional hours to cover a busy period, this may trigger the requirement to auto enrol them into the workplace pension scheme. However, postponement may be an option in this situation. Eligibility:

Read more…

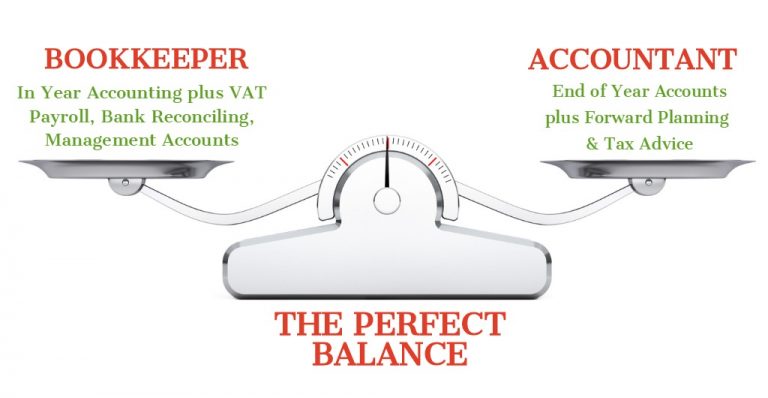

Do I need a Bookkeeper or an Accountant?

Many small business owners don’t understand the difference between a Bookkeeper and an Accountant which is understandable, as the roles are very close. The ideal solution is to have both.

What a Bookkeeper does………..

A Bookkeeper will record all past income and expense that a business has generated, often on a weekly, monthly or quarterly basis. A good bookkeeper will always reconcile business bank accounts regularly to ensure nothing is missed. VAT will be recorded, with the VAT returns calculated and submitted to HMRC as required. Payroll will be processed and entered into the bookkeeping system correctly if applicable. Regular reports will show the business owner how their business is performing with up to date information that can help them with important business decisions that may have to be made such as when and how to grow.

What an Accountant does….

An Accountant will take the figures that have been recorded by either a bookkeeper, or the business owner and prepare a set of ‘End of Year’ Financial Accounts. The figures from these End Of Year accounts will be used to calculate and submit either a self-assessment to HMRC for Sole Traders and Partnerships, or to Companies House when a business is incorporated (Limited), along with a Corporation Tax calculation. An Accountant will also help to ensure the business is taking advantage of any tax benefits that may be available and help with forward planning.

Where Bookkeepers and Accountants cross over

The crossovers happen with some bookkeepers offering end of year accounts preparation and self-assessment submissions, plus some accountants offering in-year bookkeeping, VAT returns, Payrolls and management accounts as additional services. Although this can offer the customer a one-stop shop, it’s not always the best solution. Bookkeepers are good at Bookkeeping, Accountants are great at End of Year Accounting and are equipped to offer advice on items such as tax planning.

Bookkeepers are often not as experienced as Accountants when it comes to End of Year and forward planning – and then Accountants aren’t necessarily good at doing bookkeeping!

The best solution is to have a bookkeeper doing the in-year and an Accountant doing the end of year.

This doesn’t mean it has to be expensive. A bookkeeper can save you money by:

- making sure you’re claiming everything you’re entitled to claim

- saving you the time and stress of doing this work yourself, freeing you up to earn more money doing what you’re good at.

- Giving you up to date regular reports of all your income and expense trends so that you know where the business is exceling and where it may need tweaks or improvement.

- Working closely with your Accountant, often resulting in a lower bill from them, as they know figures are correct and only need minimal checking and adjustment.

Why is Lady of Ledger Different from other Book Keepers?

Lady of Ledger has been trading since 2004 so has over 20 years of experience with many different types of professions. We are insured and licenced under the International Association of Bookkeepers. We’re a friendly team that works hard at offering a modern and plain language service.

We scan all paperwork into the accounting software, so that you, and indeed anyone else you choose to allow, will have the opportunity to view this from any internet enabled device.

We work exclusively with QuickBooks Online (QBO) software, this means we know the software inside out, and in the unlikely event there’s something we don’t know, we can liaise directly with QuickBooks – thanks to our Gold ProAdvisor status membership following our Advanced Certification Training.

Why not have a read of many of our customer testimonials – we’re very proud that many of them mention our confidence and knowledge as the main reason they chose us from others in the first place – and why they stay with us.

Read Less...

Many small business owners don’t understand the difference between a Bookkeeper and an Accountant which is understandable, as the roles are very close. The ideal solution is to have both. What a Bookkeeper does……….. A Bookkeeper will record all past income and expense that a business has generated, often on a weekly, monthly or quarterly

Read more…

How to Prepare for Making Tax Digital

If your business is VAT registered, with a rolling 12 months turnover above £90,000, did you know that it is mandatory for you to keep digital records in relation to your VAT compliance?

HMRC introduced Making Tax Digital for VAT in 2019. No longer are you able to keep your bookkeeping records in a book, on pieces of paper, or even to some degree on a spread sheet. You are no longer able to log in to the HMRC portal and file your VAT return into HMRC’s website – you are now obliged to file through accounting software such as QuickBooks Online.

How to make filing VAT digitally – easy

- Talk to your Bookkeeper or Accountant to see if your current software – if you have any – is HMRC ready. If it is, they will then need to set up the link between that software and your MTD account.

- If you still use spread sheets or manual bookkeeping, the easiest way is for you to move to a software package such as Intuit QuickBooks.

- If you are worried about using software why not speak to a bookkeeper. Many businesses find that outsourcing their bookkeeping is just one less headache for them, freeing up time and reducing the stress.

- Using an accounting software will record all of your business transactions and file your VAT return direct to HMRC. This needs to be set up and running correctly so that you ensure the amount you report to HMRC – and consequently pay – is not too much, or too little – a Bookkeeper can ensure this is done for you.

Benefits of Using Accounting Software

So is Making Tax Digital a bad thing? No, not at all! There are many benefits that the business owner can take advantage of, such as:

- Daily bank feeds allow you to see who has paid you and what’s gone out of your bank without logging into your bank each time.

- More up to date, valuable reports at the touch of a button helping you to make more informed decisions about your business. No more waiting until after year end to get this information.

- Personalised invoices can be sent to your Customers direct from the software from any internet enabled device. Ideal for those business owners on the go.

- Can be linked with payment processes such as PayPal etc, so you can allow your customer to pay with their debit or credit cards.

- Paperwork can be scanned in and attached to the transactions – meaning you no longer have to keep it, so less storage is needed.

How Much Does Accounting Software Cost?

With QuickBooks Online the monthly subscriptions vary from £10 to £40 for the majority of small business’s depending on the version you decide to go with. QuickBooks is fairly easy to learn if you want to carry out your own bookkeeping and VAT returns. For those that prefer to let a professional manage this task for them, the Online version allows both the business owner and a Bookkeeper/Accountant to access the same file remotely.

If you’re a small business owner in Telford, Shropshire and want help to convert your bookkeeping to being Making Tax Digital Compliant, contact us via email to find out more – info@ladyofledger.co.uk.

Read Less...

If your business is VAT registered, with a rolling 12 months turnover above £90,000, did you know that it is mandatory for you to keep digital records in relation to your VAT compliance? HMRC introduced Making Tax Digital for VAT in 2019. No longer are you able to keep your bookkeeping records in a book,

Read more…